You are looking at a commercial invoice and the HS code on it does not match the goods. Maybe it covers similar hardware but not this specific product. Maybe it is the code the supplier always uses regardless of what they ship. Either way, you are about to make a legally binding declaration to customs against a code you already know is wrong, and the penalty exposure lands on you, not the supplier.

A wrong HS code on the invoice is one of the most common classification problems importers face. It is also one of the most fixable, if caught early, and one of the most expensive if not: the same error is a paperwork amendment before entry, an electronic correction after clearance, a repayment or protest after the debt is notified, and, in the worst case, a compliance filing with penalty exposure. What you do depends entirely on where the shipment is in its lifecycle right now, and which country’s customs authority owns the file.

The six-digit HS code is the same in every country in the world, set by the World Customs Organization and used by all WCO members. The correction procedure is not: each customs administration has its own mechanism, form, and deadlines. This guide walks the stages of a correction, with the specific procedure for the three jurisdictions covering most trade lanes: the US, the EU, and the UK.

The Correction Decision at a Glance

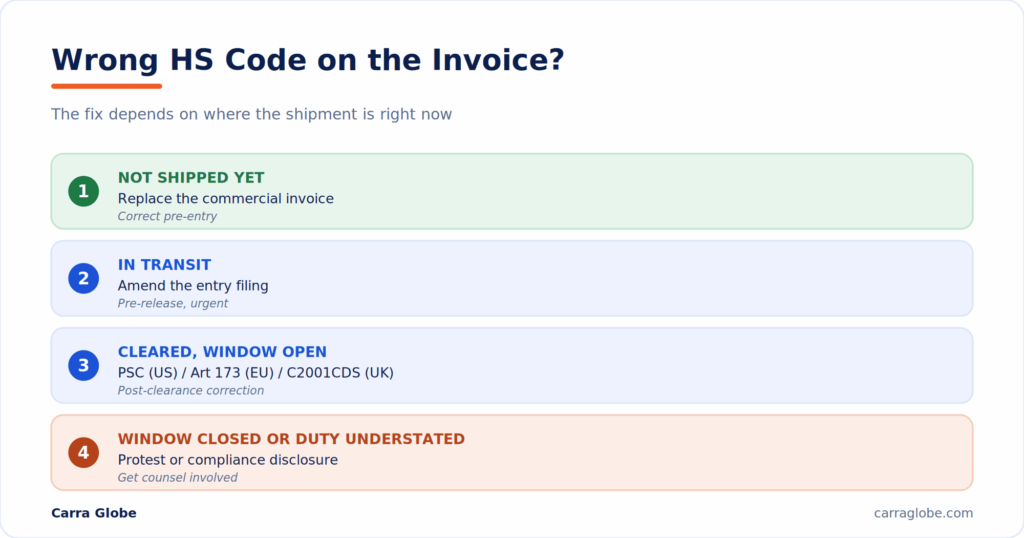

- Goods not yet shipped → replace the commercial invoice; correct pre-entry.

- Goods in transit, not yet cleared → amend the entry filing pre-release, urgently.

- Goods cleared, within the correction window → file a Post Summary Correction (US), Article 173 UCC amendment or Article 116 repayment (EU), or C2001CDS voluntary disclosure or C285CDS repayment (UK).

- Correction window closed → US protest under 19 U.S.C. 1514 within 180 days of liquidation; EU beyond the Article 116/121 UCC three-year limits and UK beyond HMRC’s three-year notification period leave only very limited administrative options.

- Wrong code understated duty on a covered tariff line → treat as compliance disclosure, not amendment, and get counsel.

First Question: Is the Code Actually Wrong, or Just Different?

Before you correct anything, confirm the code is wrong. Suppliers, brokers, and importers often disagree on classification for reasons that are not actually errors: national tariff schedules extend the six-digit HS code to eight, ten, or more digits, so a code that looks unfamiliar to you may just be a different country’s version of the right heading. And the same physical goods can classify differently depending on how they are presented, which is what our guide to the HS codes for electronics and tech equipment sets out at length.

Three checks separate a real error from a difference:

- Compare at six digits, not ten. The first six digits of the HS code are the same worldwide. If your code and the supplier’s match at six, you have a national-line disagreement, not a wrong heading.

- Test against form, function, and presentation. Ask what the item physically is, what it does, and how it ships. If the supplier’s code answers those consistently and yours does too, you may both be defensible; if one clearly does not, that is your error.

- Check the destination’s official schedule. The importing country’s tariff schedule is authoritative for its rate. Confirm the line in that jurisdiction: the US Harmonized Tariff Schedule for US imports, the EU TARIC database for the EU, and the UK Integrated Online Tariff for the UK.

For the electronics and tech-hardware categories most importers we work with are shipping, the right heading is set out in the deep-dive spoke for that product family: servers and computers (8471), chips and GPUs (8542), routers and networking (8517), lithium batteries (8507), solar panels and inverters (8541/8504), and medical devices (9018).

If the six-digit heading is wrong, or the code fails the form-function-presentation test, you have a real correction to make. The right move depends on where the shipment is right now.

If Your Supplier Used the Wrong HS Code

Suppliers tend to reuse the same HS code across their catalogue, whichever one is closest to the products they ship most often, rather than classifying each SKU individually. The habit is understandable, but the responsibility does not travel with it. Under the customs law of most major jurisdictions, the importer of record (in the US) or declarant (in the EU and UK) certifies the classification to customs and bears the penalty exposure if it is wrong, not the supplier. The correction path runs through the importer’s broker and the destination customs authority, not through a request to the supplier to reissue the paperwork alone.

Two protections belong in the commercial arrangement rather than the correction procedure. Agree the correct HS code in the purchase order in writing, so the supplier is contractually obliged to invoice it. And where high-value shipments justify it, add a classification warranty and an indemnity for duty and penalty exposure caused by supplier misclassification. The correction guide below covers what to do when those safeguards were not in place.

Stage 1: The Goods Have Not Shipped Yet

This is the easy case, and it is where most of these problems should be caught. Request a corrected commercial invoice from the supplier with the right code, and ensure the packing list and any transport documents match it before the shipment moves. Send the corrected documents to your customs broker or filer so the entry is submitted against the right classification from the start. Keep the original invoice and the correction email in your records; a paper trail showing the error was identified and fixed before entry protects you if the code is ever questioned. Do not rely on the broker to catch it silently. Brokers classify based on what the invoice says; if the invoice is wrong, the entry will be wrong unless you flag it.

Stage 2: The Goods Have Shipped, Not Cleared

Still recoverable, and speed matters. Contact your broker or customs agent immediately with the corrected classification and, if possible, a revised invoice from the supplier. In most jurisdictions the broker can amend the entry filing before customs releases the goods, or file the entry against the correct code in the first place if it has not been submitted yet. Air freight and ocean shipments are often pre-cleared or filed just before arrival, so a few hours can be the difference between fixing this on paper and fixing it after release. Pre-release amendments avoid the risk of paying a wrong duty and then having to claim it back, so if you can catch the error while the goods are in transit, treat it as urgent rather than routine.

How to Correct an HS Code After Shipment (Stage 3: Post-Clearance)

Now the shipment is in the country and the duties are paid or accrued, but the entry has not yet reached the point where the correction window closes. Every major customs administration has a formal, electronic mechanism for this stage; the names and deadlines are what change.

| Jurisdiction | Mechanism | Who Files / Where | Deadline | Penalty Position |

|---|---|---|---|---|

| United States | Post Summary Correction (PSC) | Importer of record or authorised filer, via ACE | 300 days from entry date; must be at least 15 days before scheduled liquidation | Proactive PSC generally reduces audit risk; entry must be accepted, in CBP control, not under review, and paid |

| European Union | Article 173 UCC amendment; Article 116 UCC repayment application (over-declared duty) | Declarant, to the Member State customs office where the debt was notified | 3 years from customs debt notification | National implementation varies; expect direct contact with the supervising office rather than a central portal |

| United Kingdom | Voluntary disclosure via C2001CDS (underpayment) or C285CDS (overpayment) | Declarant or agent, submitted to HMRC via CDS | 3 years from customs debt notification | Unprompted disclosure materially reduces Finance Act 2008 penalty exposure; C18 issued for the underpaid amount |

Two practitioner notes worth carrying into any post-clearance correction. First, implementation varies significantly by Member State in the EU, and in practice many Article 173 amendments are handled through the supervising customs office rather than a central portal, so early contact with the office that notified the debt saves time. The European Commission’s guidance on repayment and remission sets out the framework across the bloc. Second, HMRC’s three-year clock runs from notification of the customs debt, which is not always the entry date, and voluntary disclosure timing directly affects the penalty band under Finance Act 2008, so file promptly once the error is identified.

In every jurisdiction, the same operational rule holds: have the record ready before you file. A post-clearance correction on a classification change should be backed by, at minimum, the corrected commercial invoice or an amendment from the supplier, the product specifications supporting the correct heading, a short classification rationale walking through form, function, and presentation, any prior binding rulings you are relying on, and the broker communication chain showing when the error was identified.

Working through an HS code correction on a live entry? Carra Globe classifies, files, and manages corrections as your importer of record across 175+ countries.

Stage 4: The Correction Window Has Closed

Once the electronic correction window closes, the tools change. In the US, once the entry has liquidated, the PSC path is closed and the remaining administrative route is a protest under 19 U.S.C. 1514, filed within 180 days of the liquidation date. A protest is a formal challenge, not a routine correction, and it must identify the entry, state the grounds, and be supported by the facts. Classification is among the CBP decisions that can be protested.

In the EU, if the three-year repayment or recovery window under Articles 116 and 103 UCC has expired, options narrow to case-specific relief and the underlying customs debt generally cannot be revisited. In the UK, HMRC’s three-year notification period effectively sets the outer boundary on voluntary correction; beyond it, HMRC can no longer notify the debt, but neither can the importer easily correct it. In every jurisdiction, once the standard window is closed, any correction that involves under-declared duty or a covered tariff should be reviewed with qualified counsel before you submit anything, because the label for that filing may no longer be “correction.”

When a Correction Becomes a Disclosure

Not every wrong HS code is a clerical error. If the incorrect code understated duty, and especially if it moved the goods outside the scope of a tariff surcharge, an anti-dumping duty, or a covered trade-defence measure, the correction is a compliance matter with penalty exposure. In 2026 this happens more often than importers realise: the same server can be duty-free under one 8471 subheading and carry a 25 percent Section 232 surcharge under another, and the same solar module can be near duty-free under one origin and carry punitive AD/CVD under another. What looks like a paperwork slip on the invoice can be a materially undervalued declaration to customs.

Each jurisdiction has its own name for the corresponding voluntary-disclosure mechanism, and each carries its own penalty framework. In the US, a prior disclosure to CBP made before the agency initiates a formal investigation limits penalty exposure under 19 U.S.C. 1592. In the UK, C2001CDS is itself the voluntary-disclosure route, and the Finance Act 2008 penalty regime applies discounted rates for unprompted disclosures with careless behaviour carrying penalties of up to 30 percent of the lost revenue, and deliberate behaviour up to 70 percent. In the EU, Member State customs authorities apply the recovery procedures under Articles 101 to 105 UCC, with penalties governed by national law that varies significantly by country. And in 2026 the chance of a mismatch quietly slipping through is lower than it used to be everywhere: risk-based targeting draws on entry-level data at scale, and enforcement of tariff scope, origin, and forced-labour compliance has stepped up materially, so codes near a covered measure attract scrutiny they might have avoided a few years ago.

The threshold decision, whether to characterise the fix as a routine amendment or a compliance disclosure, is not one to make casually or unilaterally; it depends on the size of the duty variance, the pattern of the error across entries, and whether covered measures are engaged. This is where trade counsel earns its fee. The cost of getting the characterisation wrong is set out in our guide to the cost of incorrect HS codes for high-tech equipment imports.

How to Stop This Happening on the Next Shipment

Wrong codes on invoices are rarely one-off; the same supplier tends to make the same mistake shipment after shipment. Six practical steps break the pattern:

- Pre-agree the code. Confirm the correct HS heading with the supplier as part of the purchase order, in writing, before goods ship.

- Provide a product classification sheet. Give suppliers a short document listing your SKUs and the codes to use for each. Do not leave classification to whoever fills out the invoice.

- Verify at receipt of documents. Check the code on every commercial invoice against your sheet before the broker files, using our free HS Code Finder as a quick cross-check. Two minutes prevents most problems.

- Watch the constraint columns. If your goods sit near a Section 232, Section 301, AD/CVD, or export-control boundary, treat that boundary as the classification, not a footnote.

- Keep a classification file. Store the reasoning, any rulings, and the sources you relied on. If a customs authority ever asks, you want a defence ready, not a scramble.

- Consider a binding ruling for high-volume or high-value SKUs where the correct code is genuinely disputable: a CBP ruling in the US, a Binding Tariff Information (BTI) in the EU, or an Advance Tariff Ruling in the UK.

Frequently Asked Questions

Who is legally responsible for the HS code on the invoice?

The importer of record in the US, or the declarant in the EU and UK. Whatever the supplier wrote on the invoice, the party certifying the entry to customs bears the penalty exposure.

This is why the supplier’s code is a starting point, not the answer, and why a competent importer verifies every code before entry.

Can my customs broker fix the wrong HS code?

Yes for the mechanics, but only the importer of record can authorise the correction. Brokers submit the filings on the importer’s behalf; they do not decide whether or how to correct.

If the correction involves potentially understated duty or a covered tariff, the decision on how to file it belongs to the importer, informed by trade counsel.

Can you change the HS code after customs clearance?

Yes, within the destination’s post-clearance window: a PSC in the US (300 days), an Article 173 UCC amendment in the EU (3 years from debt notification), or a C2001CDS in the UK (3 years).

Filing promptly, once the error is identified, is what keeps the correction inside the amendment framework rather than pushing it into a formal challenge or disclosure route.

Will correcting a wrong HS code trigger an audit?

Usually the opposite. Proactive, prompt corrections through the proper channel generally reduce audit risk. Repeated errors, late corrections, or protests filed at the last minute increase it.

What customs looks for is a pattern of care, not a record of never making mistakes.

What if the wrong code understated the duty owed?

Treat it as a compliance matter, not a clerical fix. The right path is a prior disclosure (US), a voluntary declaration under UCC recovery rules (EU), or a C2001CDS (UK); the wrong choice carries penalties.

Get qualified counsel involved before you file anything if there is meaningful duty understatement.

A wrong HS code on a commercial invoice is a fixable problem for as long as you catch it early: replace the document before shipment, amend the entry before release, use the destination’s post-clearance correction mechanism before the window closes, or the formal challenge route after. What turns it from a fix into a case is time, and the moment the wrong code understated duty on a covered tariff line. Carra Globe classifies, files, and corrects as importer of record for tech and regulated hardware across 175+ countries, so the classification is right the first time and, when it is not, corrected through the right channel in the right jurisdiction.

Disclaimer: This guide is for informational purposes only and does not constitute legal, customs, or trade advice. Correction procedures, deadlines, and penalty regimes vary by jurisdiction, entry type, and facts, and are subject to change. The US, EU, and UK procedures described here are current at the time of writing and provided as an overview only; other jurisdictions have their own equivalent mechanisms with different rules. Always confirm the current position with the relevant customs authority, a licensed customs broker, or qualified trade counsel before filing any correction, disclosure, or protest.