The Section 122 tariff was a 10% surcharge on almost all US imports that ran for exactly 150 days, from 24 February to 24 July 2026, and then expired by operation of law. For the five months it was in force it was the single largest variable in the landed cost of importing into the United States. It is gone now, replaced the moment it lapsed by a different regime, but it has not stopped mattering: importers who paid it are sitting on two live recovery routes, and the tariff that replaced it is more complex than the flat surcharge ever was.

This guide explains what the surcharge was and where it came from, what you can still recover from the period it was collected, and how the Section 301 action that succeeded it changes the calculation now. It reflects the position as of late July 2026.

Key facts:

- Rate: a flat 10% ad valorem surcharge on almost all US imports.

- In force: 24 February 2026 to 24 July 2026, a 150-day statutory life.

- How it ended: expired at its statutory limit; Congress did not extend it.

- What replaced it: a Section 301 forced-labour action of 10% or 12.5% on products of 60 economies.

In brief:

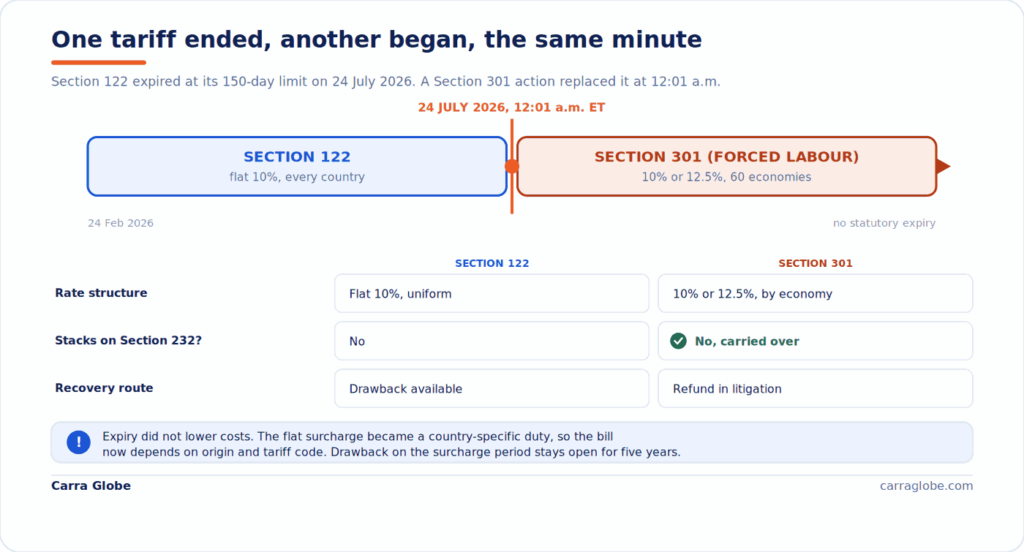

- The surcharge was a flat 10%, the same rate for every country, in force 24 February to 24 July 2026 under Section 122 of the Trade Act of 1974.

- A court ruled it unlawful, but collection continued. The Court of International Trade struck it down on 7 May 2026; the Federal Circuit stayed the injunction, so the duty was collected to its statutory expiry.

- Two recovery routes remain open. Drawback on re-exported goods survives the expiry, and refunds on the surcharge itself are still being litigated at the Federal Circuit.

- It was replaced, not removed. A Section 301 forced-labour action took effect the same moment, imposing 10% or 12.5% on products of 60 economies, subject to extensive exemptions.

- The replacement is country-specific, so the cost of importing now depends on origin and tariff classification in a way the flat surcharge never did.

Where the Section 122 Tariff Came From

The surcharge was a direct response to a Supreme Court defeat. On 20 February 2026, the Court ruled in Learning Resources, Inc. v. Trump that the International Emergency Economic Powers Act does not authorise the President to impose tariffs, which invalidated the entire IEEPA tariff structure then in place.

Within hours, the White House reached for a different and far older authority. Section 122 of the Trade Act of 1974 lets the President impose a temporary import surcharge of up to 15% to address a fundamental balance-of-payments problem. The proclamation invoked it on three grounds: a goods trade deficit of roughly 1.2 trillion dollars, a negative balance on primary income for the first time in modern history, and a net international investment position deeply in deficit. The surcharge took effect at 12:01 a.m. Eastern on 24 February 2026 at a rate of 10%.

A rise to the 15% statutory ceiling was announced the next day but never enacted, because no proclamation was ever issued to implement it. The rate that importers actually paid stayed at 10% for the whole period. The full text of the proclamation remains published on the White House proclamation page, which is the authoritative source for the exemption annexes and HTSUS assignments. For the ruling that triggered all of this, see our analysis of how the Supreme Court struck down the IEEPA tariffs.

How It Worked: Flat, Uniform, and Stacked on Some Duties

What made Section 122 distinctive, and simple to model, was its uniformity. It applied the same 10% to goods from every country. There were no country-specific rates and none of the bilateral deal reductions that had defined the IEEPA regime. India, which had negotiated a total rate of 18% under a bilateral arrangement, paid the same 10% as everyone else. The flat design was the whole character of the tariff.

The surcharge sat on top of most existing duties, and the stacking rules were where the detail lived. It applied in addition to standard MFN rates and to the existing Section 301 tariffs on Chinese goods, so a Chinese product already carrying a 25% Section 301 duty faced that plus the 10% surcharge plus its MFN rate. The one significant carve-out was Section 232: goods already subject to the national-security tariffs on steel, aluminium, copper, lumber and automobiles were excluded from the surcharge on the Section 232-covered portion.

That single distinction, stacking on Section 301 but not on Section 232, was the most important interaction rule for anyone modelling exposure, and it carried real money for importers of Chinese-origin goods in particular.

What Was Exempt

The proclamation carried a structured set of exemptions, and they remain relevant now for anyone reviewing entries from the surcharge period for a possible refund. The main categories were these.

- USMCA goods. Goods qualifying for duty-free treatment under the United States-Mexico-Canada Agreement were exempt. This was the largest single saving for North American supply chains, but it was never automatic: it had to be claimed on every entry with a valid Certificate of Origin for goods from Mexico and Canada.

- CAFTA-DR textiles and apparel. Qualifying duty-free textile and apparel goods from Costa Rica, the Dominican Republic, El Salvador, Guatemala, Honduras and Nicaragua were exempt, a structural feature new to the Section 122 proclamation.

- Section 232 goods. Products under the steel, aluminium, copper, lumber and automobile tariffs were excluded on the covered portion, with the surcharge applying only to any remainder.

- Annex II product exceptions. Roughly 1,100 HTSUS codes were exempted, covering certain critical minerals, energy products, pharmaceuticals, specified electronics, and civil aircraft parts. The list was product-code specific, so importers had to check their exact codes against the annex rather than assume a category was covered.

- Chapter 98 provisions. Goods entering duty-free under Chapter 98, such as US goods returned, were outside the surcharge, as CBP confirmed in guidance.

For IT hardware and data centre equipment, the Annex II point was the operative one. Some specified electronics fell within the exemption and some did not, and because the list worked at code level, two similar products could be treated differently. Any importer reviewing surcharge-period entries for recovery should confirm the exact HTSUS code against the annex rather than relying on the product category.

Paid the surcharge and want to know what you can recover? The two routes, drawback and the refund litigation, both turn on clean entry records for the February-to-July window. Carra Globe acts as importer of record across 175+ countries and helps importers keep entry records claim-ready and model exposure under the new Section 301 duties.

The Legal Fight, and Why It Still Matters for Refunds

The surcharge was challenged almost immediately, and the litigation is the reason a refund question is still open even though the tariff itself has expired.

On 7 May 2026, the US Court of International Trade ruled in a divided 2-1 decision that the Section 122 tariffs were unlawful, finding that the balance-of-payments conditions required to impose them were not met. The relief, though, reached only the three named plaintiffs, the State of Washington, Burlap and Barrel, and Basic Fun, so every other importer kept paying.

The government appealed, and on 12 May 2026 the Federal Circuit issued an administrative stay of the injunction pending its consideration of a longer stay. That stay held while the appeal proceeded, so collection continued from all importers right up to the statutory expiry on 24 July.

That appeal is still running. If it ultimately upholds the finding that the surcharge was unlawful, refund opportunities may open to importers beyond the original plaintiffs. If the government prevails, the duty stands. Either way there is no automatic refund channel of the kind that existed for the earlier IEEPA duties, so recovery, if it comes, is likely to depend on individual claims filed against preserved records. We track the post-expiry refund position in detail in our companion piece on what importers who paid the surcharge should do about refunds.

Recovery Route One: Drawback, Still Open

Separately from the refund litigation, there is a recovery route that does not depend on the appeal at all. CBP confirmed that drawback is available for Section 122 duties under standard procedures, and because drawback carries a five-year filing window from the date of import, this route stays open well after the tariff itself has expired.

Drawback allows recovery of up to 99% of duties paid where the imported goods are subsequently exported or destroyed. Three types apply to the surcharge.

- Manufacturing drawback, where imported goods were used as inputs in US manufacturing and the finished product was exported.

- Unused merchandise drawback, where goods imported under the surcharge were re-exported without being used, provided the export occurs within five years of import.

- Rejected merchandise drawback, where goods did not conform to specification or were defective and were returned to the foreign supplier.

For any business that paid the surcharge on goods that were later re-exported, a systematic drawback filing through ACE can recover a meaningful proportion of what was paid. This is the most reliable of the two recovery routes, because it turns on the drawback rules rather than on the uncertain outcome of the appeal. Our Global Trade Compliance team assesses drawback eligibility and manages filing for qualifying import and re-export operations.

What Replaced It: The Section 301 Forced-Labour Action

The expiry did not return costs to pre-surcharge levels, because a replacement was ready to take its place. On 23 July 2026 the US Trade Representative announced final action in a set of Section 301 investigations into forced labour, and the new duties took effect at 12:01 a.m. Eastern on 24 July, the same moment Section 122 lapsed.

The replacement is structurally different from the flat surcharge. It imposes additional duties of 10% or 12.5% on products of 60 economies, accounting for roughly 99% of US imports, rather than a single global rate. A limited set of major partners, including the European Union, Japan, South Korea, Switzerland and Taiwan, are charged a rate net of their MFN duty, meaning the Section 301 charge and the existing duty together are capped rather than stacked, and where the existing duty already meets the cap the additional rate is zero.

Two features carry over from the old regime and one is new. Goods already under Section 232 remain excluded, as they were under Section 122, and existing China Section 301 duties still apply. But unlike those older China measures, the new forced-labour duty does not stack on top of Section 232, and it comes with an extensive set of product exemptions that expanded during the comment period.

The practical result is that the cost of any given shipment now depends on its origin and its exact classification, so the flat model that worked under Section 122 no longer holds. We cover the replacement fully in our analysis of the Section 301 tariffs for 2026.

| Section 122 surcharge | Section 301 forced-labour action | |

|---|---|---|

| In force | 24 Feb to 24 July 2026 | From 24 July 2026, no statutory expiry |

| Rate | Flat 10%, every country | 10% or 12.5%, by economy |

| Scope | Almost all imports, all origins | 60 economies, roughly 99% of imports |

| Stacks on Section 232? | No | No |

| Stacks on China Section 301? | Yes | Existing China duties still apply |

| Major-partner cap | None: uniform rate | EU, Japan, Korea, Switzerland, Taiwan: net of MFN |

| Legal basis | Balance-of-payments authority | Unfair-practice authority, more durable |

What Importers Should Do Now

- Preserve every surcharge-period entry record. Retain the entry summaries and liquidation dates for all entries on which you paid the 10% surcharge between 24 February and 24 July 2026. Both recovery routes, drawback and any refund from the appeal, depend on clean records, and this is the single most important step.

- Assess drawback on anything re-exported. If any proportion of your surcharge-period imports was or will be re-exported, drawback may recover up to 99% of what you paid. The five-year window keeps this open, but the documentation has to trace back to the original import.

- Track your liquidation and protest deadlines. Refund rights tied to the appeal run on strict timelines. A post-summary correction can be filed before liquidation and a protest generally within 180 days after it, so diarise the liquidation date of every surcharge-period entry and consider protective claims while the appeal runs.

- Reclassify under the Section 301 replacement. Confirm the correct rate and any exemption for each of your product lines and origins under the new Chapter 99 provisions, so current entries are right from the first shipment. Our landed cost guide helps isolate the duty component.

- Get classification and import structure right. Accurate classification and a compliant importer of record structure protect you through legal flux and tighter enforcement, which matters more now that the applicable duty turns on precise origin and code.

This sits within a broader tightening of US customs enforcement through 2026. For the wider context, see our analysis of the 2026 customs enforcement changes affecting every importer of record.

Frequently Asked Questions

Is the Section 122 tariff still in effect?

No. The 10% surcharge expired at 12:01 a.m. Eastern on 24 July 2026 at its 150-day statutory limit, and Congress did not extend it. A Section 301 forced-labour action replaced it the same moment.

The surcharge is no longer collected on new entries. What remains open is recovery of the duty paid while it was in force.

Can I recover the Section 122 tariff I paid?

Possibly, through two routes. Drawback can recover up to 99% of duty on goods you re-exported, and is available now. Refunds on the surcharge itself depend on the appeal still running at the Federal Circuit.

There is no automatic refund channel, so preserve your entry records and track liquidation deadlines to keep both routes open.

Why was the surcharge collected after a court ruled it unlawful?

Because the Federal Circuit stayed the injunction pending appeal. A stay pauses the order’s effect, so the surcharge stayed collectable while the higher court reviewed the case, right up to its statutory expiry.

The original injunction had only ever protected the named plaintiffs, so every other importer remained liable throughout.

Did the Section 122 tariff stack on Section 301 and Section 232?

It stacked on Section 301 but not on Section 232. Chinese goods under a 25% Section 301 duty faced that plus the 10% surcharge, while goods under Section 232 were excluded on the covered portion.

That single distinction was the key interaction rule for modelling exposure while the surcharge was in force.

What replaced the Section 122 tariff?

A Section 301 forced-labour action took effect the same moment Section 122 expired, imposing 10% or 12.5% duties on products of 60 economies, subject to extensive exemptions.

It is country-specific rather than flat, and for some major partners the rate is capped net of existing duty, so model it against your own origins and codes.

What is the deadline to claim drawback on Section 122 duties?

Drawback runs on a five-year window from the date of import, not from the tariff’s expiry. So a surcharge paid in early 2026 can support a drawback claim into 2031, provided the goods were exported.

The claim must trace to the original import, so the entry records from the surcharge period are what keep the window usable.

Does the Section 301 forced-labour tariff apply to Section 232 goods?

No. Goods already covered by Section 232 duties, such as steel, aluminium, copper and vehicles, are excluded from the Section 301 forced-labour action, and the new duty does not stack on top of Section 232.

This mirrors how Section 122 treated Section 232 goods, so that carve-out carried over into the replacement.

Can I still claim drawback now that the tariff has expired?

Yes. Drawback on Section 122 duties runs on a five-year window from the date of import, so the expiry of the tariff does not close it. CBP confirmed drawback is available under standard procedures.

Manufacturing, unused merchandise, and rejected merchandise drawback all apply to goods that were subsequently exported.