The defining infrastructure story of 2026 is the construction of artificial intelligence at industrial scale, and it has a geography almost no one maps. Every AI data centre announced this year, in Texas, Abu Dhabi, Visakhapatnam, or Riyadh, depends on a physical object: an AI server packed with accelerators, memory, and networking that has to be built somewhere and physically moved to where the compute is consumed. The coverage fixates on demand, capital, and models. It rarely follows the hardware. This analysis does, because the iron law of AI server trade flows in 2026 is simple and underappreciated: if an AI server is imported into a country, it was exported from another, and the list of countries that can export it is remarkably short.

That asymmetry, many importers and very few exporters, shapes the entire build-out: who depends on whom, where the bottlenecks sit, and which governments hold leverage. This report maps it, the demand, the export nodes, the importing nations, and the control regime in between.

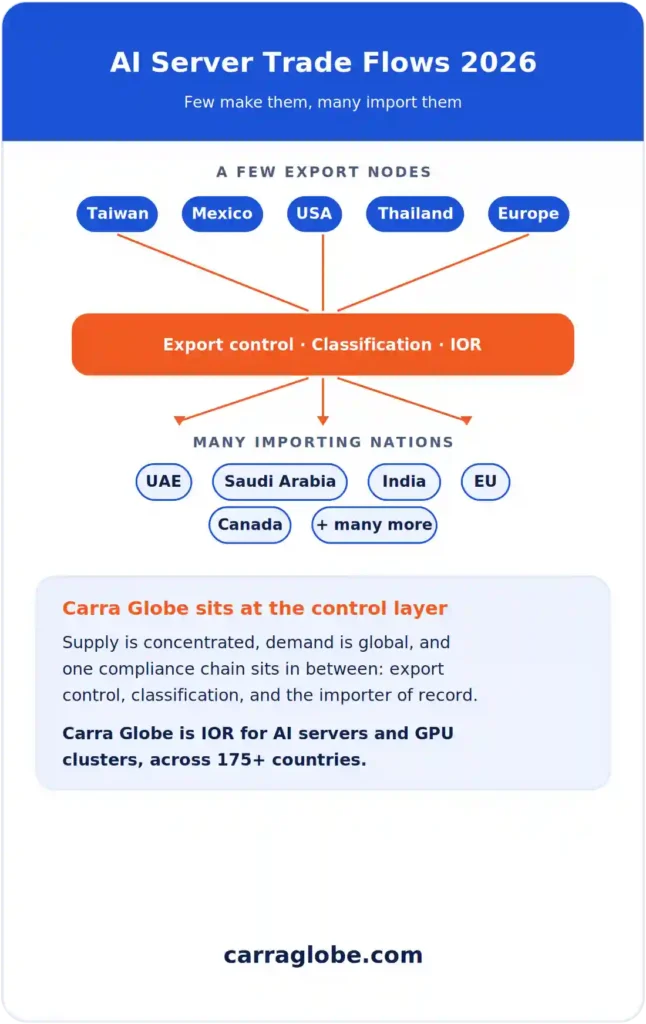

AI server trade flows in 2026 are highly asymmetric: a small number of manufacturing hubs, led by Taiwan and expanding fast in Mexico and the United States, export AI servers to a fast-growing list of importing nations across the Gulf, Europe, and Asia. Because production is concentrated and demand is global, every AI deployment is a cross-border movement governed by export controls, tariffs, and the importer of record.

The Demand: A Market Growing Faster Than Almost Any in History

Start with the scale of what has to move. The global AI server market was valued at roughly 124 to 128 billion dollars in 2024 and is forecast to reach around 850 billion dollars by 2030, a compound annual growth rate near 38 percent, among the fastest sustained expansions of any major hardware category on record. In the near term the momentum is just as stark: analysts at TrendForce expect global AI server shipments to grow more than 28 percent year on year in 2026, while total server shipments, AI and conventional combined, rise around 13 percent.

The money behind that is concentrated. The combined capital expenditure of the five largest North American cloud providers is projected to rise around 40 percent in 2026, flowing primarily into data centre construction and the servers that fill it. Within the hardware, accelerators dominate: GPU-based systems, led by NVIDIA’s Blackwell generation such as the GB200 and GB300, account for close to 70 percent of AI server shipments, while servers built on custom ASICs, including Google’s TPU and Meta’s MTIA, are rising to roughly 28 percent, the highest share in years. AMD is pushing its Instinct line, including the MI400, as the main GPU alternative. The workload mix is also shifting, from training the largest models toward inference and AI agents, which broadens demand from a few frontier labs to a much wider base of operators.

Every one of those servers, whatever the workload, has to be built in a facility capable of integrating accelerators, high-bandwidth memory, and rack-scale networking. That capability lives in very few places, which is where the map turns from demand to supply.

The Supply: Who Actually Manufactures and Exports AI Servers

Here is the part the demand coverage misses. AI servers are not made everywhere. Their assembly is dominated by a small group of Taiwanese original design manufacturers, principally Foxconn, Quanta, and Wistron through its subsidiary Wiwynn, who together handle the bulk of the world’s advanced AI server integration. These firms have transformed from notebook assemblers into the load-bearing pillars of the AI build-out: for several of them, AI servers and cloud infrastructure have overtaken consumer electronics as the largest source of revenue, with individual companies posting annual revenues above 60 billion dollars and year-on-year growth rates that doubled their business.

Crucially, where they build has shifted, and that shift is itself a trade story. To serve the United States, the largest destination, and to avoid both tariffs and security objections, these manufacturers have moved advanced server production out of China and into a spread of nodes: Taiwan itself, Mexico, the United States, Thailand, the Czech Republic, and Germany. The result is a concentrated export base. Servers destined for the US, which handle sensitive data, are now manufactured predominantly in Taiwan and Southeast Asia rather than China, a deliberate de-risking of the supply chain.

The trade statistics make the concentration visible. Taiwan’s AI server exports to the United States from January to October 2025 nearly doubled year on year, reaching around 840 billion New Taiwan dollars, and in early 2026 US imports from Taiwan exceeded imports from China for the first time in decades, driven by a surge in advanced systems. Mexico has become the other great node: its exports of automatic data processing machines, the customs category that captures servers, more than doubled in a year to exceed 85 billion dollars in 2025, according to Federal Reserve Bank of Dallas analysis, as Taiwanese manufacturers built out facilities in Guadalajara, Monterrey, and Juarez, including what is described as the world’s largest assembly site for NVIDIA’s GB200 Blackwell superchips. We examine the controls layer of this in our guide to importer of record for semiconductor manufacturing equipment.

| Export Node | Role in AI Server Supply |

|---|---|

| Taiwan | Primary design and assembly base; the dominant ODMs are Taiwanese |

| Mexico | Fastest-growing node for US-bound servers; HS 8471 exports above 85 billion dollars in 2025 |

| United States | Domestic assembly expanding to serve North American demand and hedge tariff risk |

| Thailand | Growing Southeast Asian assembly capacity for the major ODMs |

| Czech Republic and Germany | European assembly and distribution nodes serving EU demand |

Key AI Server Trade Flow Takeaways

- Manufacturing is concentrated. A small group of Taiwanese ODMs, principally Foxconn, Quanta, and Wistron, assemble most of the world’s advanced AI servers.

- Production moved out of China. Advanced server output shifted to Taiwan, Mexico, the United States, Thailand, and parts of Europe to reduce tariff and security risk.

- Mexico is the fastest-growing node. Its HS 8471 exports more than doubled to exceed 85 billion dollars in 2025.

- The US is now Taiwan-supplied. US imports from Taiwan overtook imports from China for the first time in decades, driven by advanced AI systems.

- Demand is global, supply is not. Importing nations across the Gulf, Asia, and Europe depend on this short list of export nodes.

Moving AI infrastructure across borders? Carra Globe acts as importer of record for AI servers and GPU clusters across more than 175 countries, handling export-control screening, classification, and clearance at both ends of the flow.

The Destinations: Who Is Importing the World’s AI Compute

If the export base is narrow, the import base is widening fast, and 2026 is the year sovereign AI turned from rhetoric into hardware orders. A pattern has emerged: a national fund, a cloud or telecom partner, an allocation of accelerators, and a data-sovereignty mandate. The destinations fall into a few clear groups.

The Gulf is the most aggressive importer. The United Arab Emirates and Saudi Arabia have announced combined AI infrastructure investments exceeding 100 billion dollars. Saudi Arabia’s state-backed compute champion is building toward a portfolio of data centres measured in thousands of megawatts and powered by several hundred thousand accelerators, while the UAE is constructing one of the largest AI campuses outside the United States and has signed direct deals for tens of thousands of next-generation GPUs. Both depend entirely on imported hardware, and both sit in a licensing tier that requires US government authorisation for the most advanced chips, making their imports a matter of government-to-government arrangement.

Asia outside the manufacturing nodes is the second great destination. India is building gigawatt-scale AI hubs through partnerships that pair global cloud and chip firms with domestic operators, deploying thousands of the latest accelerators, and it holds an unrestricted position under US export tiers that gives it an structural advantage in sourcing. Across the region, national AI programmes are converting public funding into GPU orders.

Europe and Canada form the third group, channelling large public commitments, a multi-billion-euro gigafactory programme in the EU and a national sovereign-compute fund in Canada, into domestic AI capacity that still runs on imported servers. Even where Europe assembles hardware, the highest-value accelerators come from elsewhere. What unites the Gulf, Asia, and Europe is not how much they buy but that none of them can make the top-end silicon at home, so each order becomes an import.

The Control Layer: Why Every AI Server Shipment Is Governed

This is where the trade flow becomes a compliance problem. Because advanced AI hardware is strategically sensitive, the leading exporter, the United States, governs where its technology can go through a tiered export-control system. Some destinations have effectively unrestricted access, others require licences for the most capable chips, and some are barred. The effect is that an AI server cannot simply be sold to the highest bidder. The destination, the end user, and the end use all have to clear the control regime before the hardware moves, and the largest sovereign buyers have had to negotiate national-level arrangements, complete with security conditions and oversight, to obtain their allocations.

The stakes of getting this wrong are not theoretical. The same period has seen enforcement actions and investigations into the diversion of controlled accelerators through intermediary countries, and proposals to tighten the rules further. For any legitimate importer, that enforcement environment raises the bar: the paperwork, the licensing, and the accountability for the import all have to be correct, because the scrutiny on advanced compute is intense and rising. We analyse the broader enforcement shift in our 2026 importer of record landscape report, and the specific control discipline in our guide to ITAR and EAR compliance for IT hardware.

Layered on top of controls are tariffs and classification. AI servers move under customs classifications that determine duty and treatment, and the tariff landscape of 2026, with new surcharges and shifting trade-defence measures, means the cost and legality of a shipment turn on getting the classification and origin exactly right. A server manufactured in Mexico, assembled from components made across Asia, and destined for the Gulf passes through several jurisdictions of rules before it powers a single model.

AI Server Trade Flows in 2026: The Compliance Reality of a Shipment

Pull the map of AI server trade flows in 2026 together and the operational picture is clear. An AI deployment in an importing country is the final step of a chain that begins in one of a few manufacturing nodes, crosses at least one border, and passes through an export-control screen, a customs classification, a duty assessment, and a legally accountable importer of record at the destination. Every one of those steps can stop the hardware.

- Origin determines exposure. Where the server was manufactured sets its tariff treatment and its export-control path.

- Destination determines licensing. The importing country’s tier decides whether a licence is needed for the most advanced chips.

- Classification determines duty. The customs code assigned to the server drives the duty owed and flags any controls.

- The importer of record carries the liability. A legally accountable party at the destination must file the entry, pay the duty, and answer for compliance.

This is why the AI build-out is, beneath the headlines about models and capital, a logistics and compliance story. The nations importing compute need a way to bring it in that satisfies the export regime at origin and the customs and accountability rules at destination. That is precisely the role of a sector-aware importer of record operating across both ends of the flow, set out in our guide to the importer of record for data centre equipment.

Frequently Asked Questions

Which countries manufacture and export the most AI servers?

Taiwan leads, through Foxconn, Quanta, and Wistron, followed by Mexico and the United States. Production shifted out of China to reduce tariff and security risk.

This concentration means most of the world’s AI compute originates from a short list of export nodes, so nearly every importing country depends on hardware made in one of them.

Which countries are importing the most AI infrastructure in 2026?

The Gulf states, led by the UAE and Saudi Arabia, are the most aggressive importers, with combined commitments above 100 billion dollars. India, the EU, and Canada are also major importers.

All of them depend on imported servers, because the ability to manufacture advanced AI hardware sits outside their borders, in the small group of export nodes.

Why are AI server exports controlled by governments?

Because advanced AI chips are strategically sensitive, the main exporting country governs where they can go through a tiered export-control system, with some destinations unrestricted, some needing licences, and some barred.

This means an AI server cannot simply be sold anywhere. The destination and end use must clear the control regime first, which is why large buyers negotiate national-level arrangements for access.

Why is importing an AI server a compliance event, not just a purchase?

Because every AI server crosses a border, it must pass an export-control screen at origin, a customs classification and duty assessment, and a legally accountable importer of record at destination. Any one can stop it.

The concentration of manufacturing means the import always traces to a foreign export node, so the compliance chain spans at least two jurisdictions and must be handled correctly at both ends.

The story of AI in 2026 is usually told through models and money. Underneath it is a story of physical hardware moving across a handful of borders under one of the most tightly governed trade regimes in the world. A few nodes export, a growing list of nations import, and between them sits a compliance chain that decides whether the compute arrives at all. Understanding that chain is becoming as strategic as the capital and the chips themselves.

Carra Globe works at that layer, acting as importer of record for AI servers and GPU clusters across more than 175 countries.

Disclaimer: This analysis is for informational purposes only and does not constitute legal, customs, or trade advice. Market figures, trade statistics, and export-control rules are complex, change frequently, and are summarised here from publicly reported information at the time of writing. Always verify current requirements and data with the relevant authority or qualified counsel.