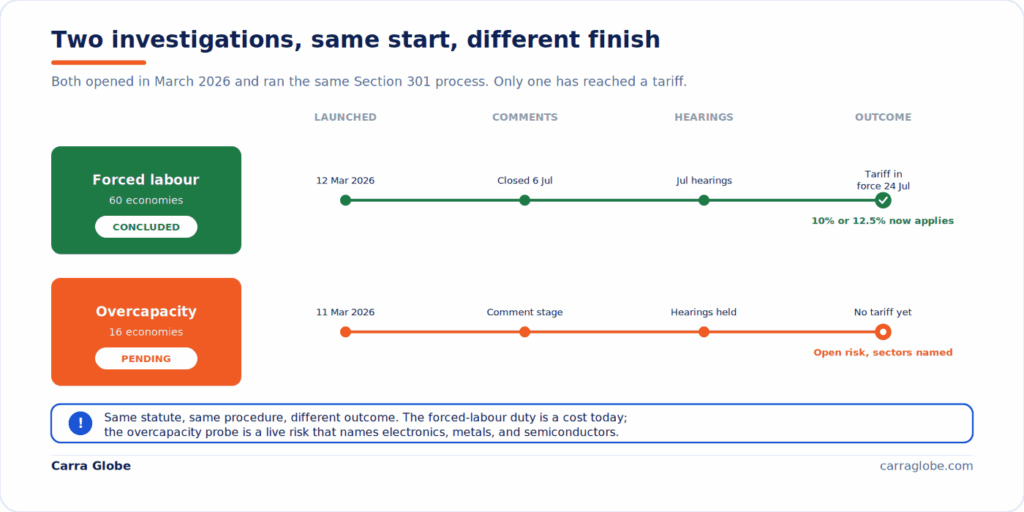

Update, 28 July 2026: One of the two 2026 Section 301 investigations has now concluded in a tariff. The forced-labour investigation of 60 economies produced a final action that took effect at 12:01 a.m. Eastern on 24 July 2026, at 10% or 12.5%, replacing the expired Section 122 surcharge. The overcapacity investigation of 16 economies has not yet produced a tariff and remains open. This guide explains both investigations, what the forced-labour one concluded, and why the overcapacity one is the risk still to watch, particularly for electronics and industrial goods.

On 11 and 12 March 2026, the Office of the United States Trade Representative launched two of the most consequential sets of trade investigations in a generation. The first targets 16 major economies for structural manufacturing overcapacity. The second targeted 60 economies for failure to enforce prohibitions on goods produced with forced labour.

Their connection to Section 122, the 10% global surcharge that ran until 24 July, was explicit: Ambassador Jamieson Greer stated that he intended to conclude the investigations before Section 122 expired, and for the forced-labour probe he did. Section 122 was temporary and capped at 15% by statute. Section 301 tariffs have no expiry and no rate cap, so this was never simply a technical transition. It was the replacement of a temporary surcharge with a durable, litigation-resistant tariff architecture.

Section 301 Investigations 2026: At a Glance

- Two separate probes: one into industrial overcapacity across 16 economies, one into forced-labour enforcement across 60.

- One concluded: the forced-labour action took effect 24 July 2026 at 10% or 12.5%, replacing Section 122.

- One pending: the overcapacity investigation has produced no tariffs yet and remains the open risk for electronics, metals, and industrial goods.

- USMCA goods exempt: qualifying Canada and Mexico goods are exempt from the forced-labour action, contrary to earlier speculation.

- Section 232 goods exempt: goods already under Section 232 do not carry the new forced-labour duty.

The Two Parallel Investigations: Structure, Countries and Sectors

The two investigations are legally distinct, procedurally parallel, and commercially interrelated. Both were initiated under Section 301(b) of the Trade Act of 1974, which authorises USTR to investigate foreign acts, policies, and practices that are unreasonable or discriminatory and burden or restrict US commerce. Details are on the official USTR Section 301 investigations page.

Investigation 1: Structural Excess Capacity (16 Economies, Still Pending)

Initiated 11 March 2026. USTR is investigating whether the acts, policies, and practices of 16 major economies create structural manufacturing overcapacity that burdens US commerce. The 16 economies are China, the European Union, Singapore, Switzerland, Norway, Indonesia, Malaysia, Cambodia, Thailand, South Korea, Vietnam, Taiwan, Bangladesh, Mexico, Japan, and India. This investigation has not yet produced tariffs, and it is the one that matters most for technology and industrial importers, because it names electronics and semiconductors directly.

The investigation examines overcapacity across seven manufacturing sectors: steel, aluminium and other metals; automobiles and parts; batteries and critical-minerals technologies; semiconductors and advanced electronics; industrial machinery, robotics and advanced manufacturing equipment; chemicals, plastics and construction materials; and solar modules and other renewable-energy components.

USTR’s theory is that government-supported overbuilding in these sectors, backed by subsidies, state-linked financing, and preferential regulation, depresses global prices and undercuts US producers. If the investigation produces a duty, it would be a separate action from the forced-labour one, carrying no obligation to repeat that action’s exemptions, and could land on the very goods the forced-labour action exempts.

Investigation 2: Forced Labour Enforcement (60 Economies, Concluded)

Initiated 12 March 2026, this is the investigation that produced the tariff now in force. USTR examined whether 60 economies fail to impose and effectively enforce prohibitions on the importation of goods produced with forced labour, framing the failure as an unreasonable practice that gives a cost advantage burdening US commerce. The legal backdrop is Section 307 of the Tariff Act of 1930, which has prohibited forced-labour imports into the United States for almost a century.

The final action took effect on 24 July 2026 at 10% or 12.5% depending on each economy’s forced-labour regime. The United Kingdom, India, Canada, and Mexico sit in the 10% tier; China and Vietnam pay 12.5%; and the European Union, Taiwan, Japan, South Korea and Switzerland are charged net of their MFN duty. Goods under Section 232, and USMCA-qualifying goods from Canada and Mexico, are exempt. We cover the rates and costs in detail in our guide to the Section 301 tariffs for 2026, and the IT-hardware angle in our analysis of the Section 301 electronics exemption.

Why Section 301 Matters More Than IEEPA or Section 122

The reason this replacement is more durable than what came before is structural. IEEPA tariffs were struck down because IEEPA does not authorise tariffs. Section 122 expired because it caps surcharges at 150 days. Section 301 tariffs, once imposed after a completed investigation, have neither constraint. Five features set them apart.

- Permanent until affirmatively removed. The original 2018 China Section 301 tariffs are still in force in 2026, eight years on. A new action begins on the same footing.

- Uncapped by statute. Section 122 was limited to 15%. Section 301 has no rate cap, though the forced-labour action landed well below that ceiling at 10% or 12.5%.

- Country and sector specific. Rather than a flat global rate, Section 301 can differentiate by country and sector, as the forced-labour tiers already show.

- Litigation resistant. A formal investigation, comment process, and documented findings create an administrative record that is much harder to challenge than the thin IEEPA basis the Supreme Court rejected.

- Stackable. Section 301 duties stack on MFN rates, AD/CVD, and other measures, though the forced-labour action notably does not stack on Section 232.

Need to know your exposure across both investigations? Carra Globe assesses Section 301 exposure across all 16 overcapacity and 60 forced-labour economies, models landed cost under the action in force and the one still pending, and confirms compliant import capability in any new sourcing corridor. We act as importer of record across 175+ countries.

Which Importers Face the Highest Overcapacity Exposure

With the forced-labour action settled, the exposure that remains open sits in the overcapacity investigation’s seven sectors. Importers sourcing these categories from any of the 16 named economies face the highest risk if that investigation produces a duty. The table shows the sectors and their highest-risk origins, alongside the existing China Section 301 exposure that already applies.

| Sector | Highest-risk origins | Existing China 301 |

|---|---|---|

| Steel and metals | China, Vietnam, India, South Korea | 25% on Chinese goods |

| Automotive and parts | China, Mexico, Japan, South Korea, India | 25% Chinese, plus 232 on steel content |

| Batteries and critical minerals | China, Indonesia, Malaysia, South Korea | 25% Chinese components |

| Semiconductors and electronics | Taiwan, South Korea, China, Malaysia, Vietnam | 25% Chinese semiconductors |

| Solar and renewables | China, Vietnam, Cambodia, Malaysia, Thailand | 25% Chinese, AD/CVD on several SEA origins |

| Industrial machinery | China, Japan, Germany (EU), Taiwan | 25% Chinese machinery |

| Chemicals and plastics | China, South Korea, India, EU | 25% Chinese chemicals |

USTR’s initiation notice names roughly 20 sectors, including cement, glass, paper, satellites, robotics, ships, and processed foods. The seven categories above consolidate them into the groupings most relevant to technology and industrial importers for planning purposes.

Where the Overcapacity Investigation Could Go From Here

With the forced-labour action concluded, the live question is what the overcapacity investigation produces. Three paths are plausible, and importers in the seven sectors should hold a response to each.

- A separate overcapacity tariff. USTR finds violations and imposes new duties on some or all of the 16 economies and seven sectors, country and sector specific. This would stack on existing measures and, unlike the forced-labour action, carries no guarantee of matching its exemptions. Importers in targeted sectors should treat this as the primary planning case.

- Negotiated forbearance. USTR uses the findings as leverage, and trading partners commit to policy changes in exchange for holding tariffs back. Several named economies are pursuing this through diplomatic channels, but the investigation record and USTR’s authority remain in place, making such arrangements fragile.

- A prolonged investigation. The overcapacity probe runs on without a near-term duty. This produces the lowest short-term cost but the least certainty, since an action could still follow, forcing a second adjustment for anyone who restructured around a gap.

What Importers Should Do Now

- Map every corridor against both investigation lists. For each sourcing country, confirm whether it is in the overcapacity 16, the forced-labour 60, or both. For each product, confirm whether it falls in the seven overcapacity sectors. This produces your Section 301 exposure matrix.

- Reconcile your position under the forced-labour action. Confirm the correct rate and any exemption for each product line and origin under the Chapter 99 provisions now in force. Check USMCA and Section 232 eligibility, since both fully exempt qualifying goods. Our landed cost guide sets out the full duty stack.

- Model the overcapacity scenario as your open risk. For high-exposure corridors, model landed cost if an overcapacity duty lands, benchmarking against the existing China Section 301 rates as a guide to what a sector-specific action can reach. Engage early if a proposed action appears.

- Review your IOR structure in every affected corridor. If a future action reshapes your optimal sourcing, the import compliance infrastructure in any new corridor must be confirmed before the first shipment, and entity or certification timelines can run to months. For the role itself, see our explainer on what an Importer of Record does.

How Carra Globe Supports Importers Through the Section 301 Investigations

Carra Globe provides Global Trade Compliance covering Section 301 exposure assessment across all 16 overcapacity and 60 forced-labour economies, with landed cost scenario modelling for both the action in force and the one still pending.

Our Importer of Record service is active across the full investigation country set, providing compliant import capability in any new sourcing corridor without the delay of entity establishment.

For the wider landscape, see our guides to the SCOTUS IEEPA ruling and the Section 122 tariff.

Frequently Asked Questions: Section 301 Investigations 2026

What is the status of the Section 301 investigations in 2026?

The forced-labour investigation of 60 economies concluded in a tariff, effective 24 July 2026 at 10% or 12.5%. The overcapacity investigation of 16 economies is still open, with no tariff yet.

The overcapacity probe names electronics, semiconductors, metals, and other sectors, so it remains the live risk for importers in those categories.

Which countries are under the overcapacity Section 301 investigation?

China, the EU, Singapore, Switzerland, Norway, Indonesia, Malaysia, Cambodia, Thailand, South Korea, Vietnam, Taiwan, Bangladesh, Mexico, Japan, and India. Sixteen economies across seven manufacturing sectors.

The sectors are steel and metals, automotive, batteries and critical minerals, semiconductors, solar and renewables, industrial machinery, and chemicals and plastics.

What sectors are in the Section 301 overcapacity investigation?

USTR’s notice names roughly 20 manufacturing sectors, including steel and metals, automobiles, batteries and critical minerals, semiconductors and electronics, solar and renewables, industrial machinery, and chemicals and plastics.

Others named include cement, glass, paper, robotics, satellites, and ships. Importers sourcing any of these from the 16 named economies face the highest overcapacity exposure.

Do the new Section 301 tariffs stack on existing duties?

Yes, with one exception. Section 301 duties stack on MFN rates, existing China Section 301 tariffs, AD/CVD, and other measures. The forced-labour action, though, does not stack on Section 232.

For Chinese goods, the new 12.5% forced-labour duty applies in addition to the existing Section 301 rates in place since 2018, plus the MFN rate.

How is the forced-labour investigation different from the UFLPA?

The UFLPA creates a rebuttable presumption that goods from Xinjiang are made with forced labour. The Section 301 forced-labour action is broader: it targets 60 economies’ failure to enforce their own forced-labour import bans.

The UFLPA targets specific goods from a specific region. The Section 301 action targets government-level enforcement failures across 60 countries and reaches a far wider range of goods and origins.

Are USMCA goods exempt from the Section 301 forced-labour tariff?

Yes. Qualifying goods from Canada and Mexico entered duty-free under USMCA are exempt from the forced-labour action, under specific HTSUS headings. Earlier speculation that USMCA status would not carry over proved incorrect.

Mexico is still named in the pending overcapacity investigation, though, so USMCA exemption from the forced-labour duty does not shield it from a possible future overcapacity action.

Could the overcapacity investigation still produce tariffs?

Yes. The overcapacity investigation of 16 economies remains open and has not concluded. If USTR finds violations, it could impose a separate, country and sector-specific duty on the seven named sectors.

It carries no obligation to repeat the forced-labour action’s exemptions, so it could land on electronics and industrial goods that the forced-labour action exempts. Model it as an open scenario.

Of the two Section 301 investigations launched in March, one is now a duty importers pay and one is a risk that has not materialised. The forced-labour action landed at 10% or 12.5%, with USMCA and Section 232 goods exempt, and the overcapacity investigation, which names electronics and semiconductors, is the one still to watch. The importers who handle this well reconcile their position under the action in force and keep modelling the one still open. If you would like that done across your corridors, Carra Globe acts as importer of record across 175+ countries and can help you put it in place.