In 2026, a reseller sells a client a data centre buildout: servers, GPU clusters, switching, and the power hardware to run it, shipped to another country. The client wants it delivered, installed, and live. Simple enough as a sale, until the goods reach the destination border and customs asks the question that stops the shipment: who is the importer of record, and who is legally liable if anything on the declaration is wrong? For value-added resellers, systems integrators, and ITAD firms moving high-value, regulated hardware (IT and AI infrastructure, medical devices, telecom equipment) across borders, this is the question that decides whether a deal is profitable or becomes a compliance liability that outlives the invoice.

The reseller sits in the middle of a three-party chain (supplier, reseller, end client), and that middle position is exactly what makes the liability question harder than a normal import.

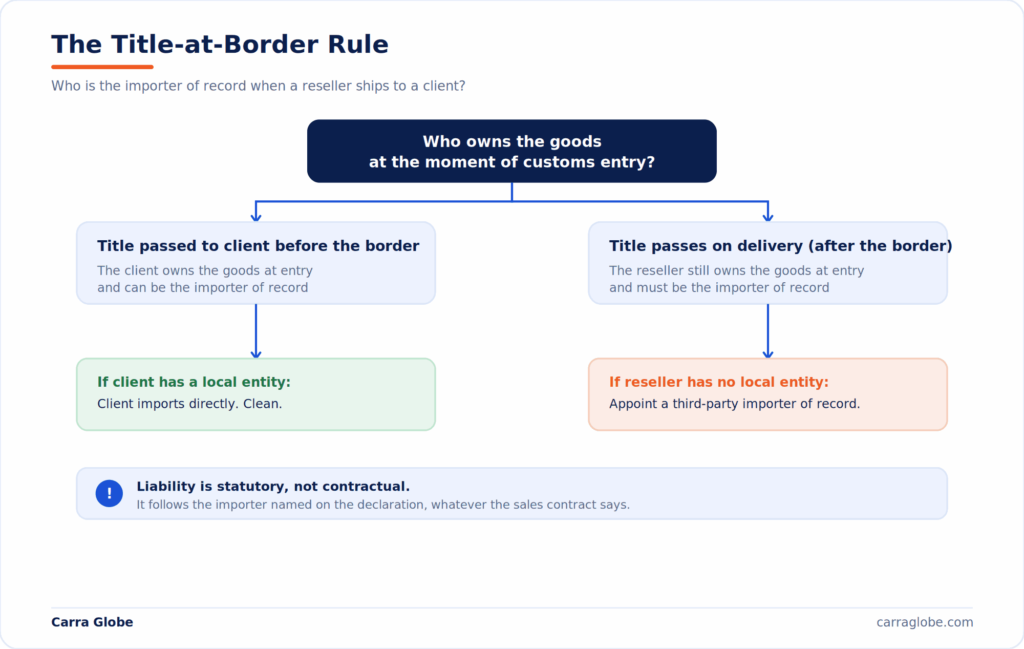

When a reseller ships hardware to a client abroad, the importer of record is whichever party holds legal title to the goods at the moment of customs entry, and that party carries the liability. If the client does not take title until after delivery, only the reseller (or a third-party importer of record acting for the reseller) can legally be the importer. If title passes to the client before the border, the client can be the importer, but only if they have a registered entity in the destination country. This is the Title-at-Border Rule, and the liability that comes with it is statutory: it follows the importer of record named on the declaration, not the commercial contract between the parties.

Who is liable when a reseller imports hardware for a client?

Most explanations of import liability assume two parties: a buyer importing goods for their own use, and the logistics providers who move them. The reseller scenario breaks that model, because the goods change ownership on their way to the border. The supplier sells to the reseller. The reseller sells to the end client. Somewhere in that chain, legal title passes, and where it passes determines who customs treats as the importer.

This matters because the importer of record role is not a commercial choice the parties can freely assign. Customs authorities in most jurisdictions define the party entitled to make entry as the owner, the purchaser, or their authorised agent, so the entry has to name whoever legally owns the goods at that point. In the US, CBP’s importer identity requirements set out who may be named. When the paperwork names a party who does not, the shipment stops.

The reseller’s position also carries a risk the end client does not share: the reseller often never physically handles the goods. The hardware may ship directly from the supplier’s warehouse to the client’s site, with the reseller involved only on paper. That drop-ship structure is efficient, but it means the reseller can be named as importer of record, and carry full liability, for goods they never saw, inspected, or classified. Getting this wrong can leave a reseller owing duties, penalties, and back-taxes, and exposed to a compliance investigation, on hardware they never physically handled. The liability is real even when the involvement is purely contractual.

Why Title at the Border Decides Everything

The Title-at-Border Rule turns on one contract term: when legal title passes to the end client. That term is set by the terms of sale, and it has consequences most resellers do not anticipate.

If the client takes title only on delivery, after the goods have cleared customs, then the client does not own the goods at the moment of entry. Under the customs law of many countries, only the owner at the time of importation can act as the importer of record. That means the reseller, who still owns the goods as they cross the border, is the party who must be the importer, or must appoint someone to be the importer on their behalf. The client cannot be named as importer of record for goods they do not yet own.

If ownership passes to the client before the border, at the supplier’s dock, or at the port of origin, then the client owns the goods at entry and can be the importer of record, provided they have a registered legal entity in the destination country. If they do not have that entity, ownership does not help them: they still cannot file the entry, and the shipment needs another solution.

This is the trap. Resellers often assume that because the client is the final buyer and the goods are going to the client’s site, the client is automatically the importer. That assumption fails on both counts: the client may not own the goods at entry, and even if they do, they may have no entity to import through. When either is true, the liability lands back on the reseller.

A concrete example makes it clear. A UK reseller sells fifty servers to a client in Brazil. Their sales contract says title passes to the client on delivery, which is standard. That single clause means the UK reseller still owns the goods when they arrive at the Brazilian border, so under Brazilian import law the reseller, not the client, must be the importer of record. But the UK reseller has no Brazilian entity and cannot file an entry in Brazil. The client, who does have a local presence, cannot be the importer either, because they do not yet own the goods. Neither party can lawfully import, and the shipment stalls, until the reseller appoints a third-party importer of record with a Brazilian entity to take the role, the exact structure covered in our guide to shipping IT hardware to Brazil without a local entity. Change one detail, make title pass at the UK warehouse instead, and the answer flips: now the client owns the goods at the border and can import in Brazil on their own entity. The contract clause, not the logistics, decided who was liable.

The principle is consistent across jurisdictions, though the detail varies. In the United States, CBP recognises the owner, purchaser, or consignee as eligible to be the importer of record, so a reseller holding title at entry qualifies, but a foreign reseller with no US presence still needs a resident importer or a third-party IOR. In the European Union, Article 170 of the Union Customs Code requires the declarant to be established in the customs territory, which is a harder barrier: a non-EU reseller usually cannot be the importer at all without an EU-established entity acting as, or on behalf of, the declarant. The ownership question decides who should be the importer; local establishment rules then decide whether they can be.

What the Importer of Record Is Actually Liable For

Being named importer of record is not an administrative formality. It is a legal liability position fixed by law, and the exposure is open-ended. Whoever holds the role, reseller or client, is legally accountable for the following:

- Classification accuracy. If the HS code is wrong and the goods were subject to a higher duty or an anti-dumping measure, the importer owes the difference plus penalties. Our guide on a wrong HS code on the invoice covers how those corrections work.

- Declared value. If the value is understated, the importer of record faces a customs undervaluation investigation, not the supplier who set the price.

- Duties and taxes. The importer pays them, and remains liable for any shortfall found later.

- Licences and certifications. For IT hardware, this can include type approvals, encryption declarations, and dual-use export-control compliance. The importer holds the exposure if any are missing.

- Post-clearance audit. Liability does not end at release. Customs authorities run audits for years afterward, and back-duties and penalties land on the importer of record of the original entry.

The critical point for resellers: this liability is statutory, not contractual. A reseller cannot sign it away to the client in the sales agreement. The client and reseller can agree between themselves about who reimburses whom, but customs pursues the party named on the declaration regardless of any private arrangement. If the reseller is the importer of record, the reseller is who customs comes to, whatever the contract says.

The Reseller’s Three Options

Faced with a cross-border sale, a reseller has three realistic ways to structure the import, each with a different liability outcome, and the Title-at-Border Rule decides which ones are even available.

| Option | Who is the importer of record | What it requires | Who carries the liability |

|---|---|---|---|

| 1. Client imports | End client | Client holds title at the border and has a registered local entity | End client |

| 2. Reseller imports | Reseller | Reseller has a registered entity in the destination country | Reseller |

| 3. Third-party IOR | Specialist IOR | None from reseller or client: the IOR provides the local entity | Third-party IOR |

Option 1: Make the client the importer of record

This shifts the liability to the client, and it works only if two conditions are met: title passes to the client before the border, and the client has a registered entity in the destination country. When both hold, this is clean. The problem is that clients frequently resist taking on importer liability, especially for IT hardware with complex compliance requirements, and many clients have no local entity in the market where they want the goods delivered. When either condition fails, this option is off the table.

Option 2: Become the importer of record yourself

The reseller takes on the importer role directly. This is only possible if the reseller has a registered entity in the destination country, with the customs registration, tax identification, and import licences that role requires. For a reseller shipping into one home market, this can be viable. For a reseller selling into multiple countries, it means establishing an entity in each one, which is slow, expensive, and rarely justified by a single deal. And it puts the full legal liability on the reseller, including the classification and valuation of goods they may never have physically handled.

Option 3: Appoint a third-party importer of record

The reseller appoints a specialist importer of record that holds registered entities in the destination country. The third-party IOR files the entry in its own name, pays the duties, manages the certifications, and carries the customs liability, while the goods are delivered to the client as consignee. This is how most cross-border reseller deals actually work, because it removes the need for either the reseller or the client to have a local entity, and it places the compliance exposure with a party equipped to carry it. Our guide on how to choose an importer of record covers what to look for in that provider. The reseller remains the commercial owner of the transaction; the IOR takes the regulatory role. Our guide on how to import IT equipment without a local entity covers this structure in full.

Reselling IT hardware into a market where neither you nor your client has an entity? Carra Globe acts as the importer of record on your behalf, filing the entry, paying duties, and carrying the customs liability, while your client receives the hardware as consignee, across 175+ countries.

How This Differs From the Other Import Roles

The reseller scenario is often confused with adjacent role questions, but it is distinct from each. The reseller is not a freight forwarder, and the difference in liability is total: a forwarder moves the goods and carries no customs liability, while the importer of record carries all of it. That distinction is set out in our guide to freight forwarder versus importer of record. The reseller is also not the same as a customs broker, who files entries as an agent without becoming the liable party, covered in our guide to importer of record versus customs broker. And the client receiving the goods is the consignee, a role distinct from the importer of record, explained in our guide to importer of record versus consignee.

What makes the reseller case unique is the ownership chain. In a straightforward import, one party buys goods and imports them for their own use, so ownership and importer status sit together naturally. In a reseller transaction, ownership moves through the chain, and the importer of record has to be whoever holds title at the border. That is the question no other role comparison answers, and it is the one resellers have to get right.

Frequently Asked Questions

Is the reseller or the end client the importer of record?

It depends on who owns the goods at customs entry. If the client takes title only on delivery, the reseller is the importer. If title passes earlier and the client has an entity, the client is.

The importer of record role follows legal ownership at entry, not the final commercial destination of the goods.

Can a reseller pass import liability to the client in the contract?

No. Import liability is statutory and follows the importer of record named on the declaration. A reseller and client can agree who reimburses duties, but customs pursues the named importer regardless of any private arrangement.

Contracts allocate cost between parties. They do not move statutory customs liability.

Does a reseller need a local entity to import for a client?

To be the importer themselves, yes, they need a registered entity in the destination country. Otherwise, the reseller can appoint a third-party importer of record that holds the local entity and carries the liability.

This is why most cross-border reseller deals use a third-party IOR rather than local incorporation.

What if the reseller never handles the goods physically?

The liability is identical. In a drop-ship arrangement where goods move directly from supplier to client, the reseller can still be named importer of record and carry full liability for hardware they never physically inspected.

Contractual involvement alone is enough to create importer liability. Physical possession is not required.

For a reseller, the liability question comes down to the Title-at-Border Rule: who owns the goods when they cross the border. Get that wrong, name a client as importer when they have no title or no entity, and the shipment stops or the liability boomerangs back to the reseller. Get it right, and the deal moves cleanly. The structure that resolves it for most cross-border reseller transactions is a third-party importer of record, which lets the reseller sell into any market without holding a local entity and without carrying open-ended customs liability. Carra Globe acts as importer of record for resellers and distributors shipping IT and data centre hardware across 175+ countries, so the goods reach the client and the liability sits where it belongs.

Disclaimer: This guide is for informational purposes only and does not constitute legal, customs, or trade advice. The rules on who may act as importer of record, and how legal title interacts with import law, vary by country and by the specific terms of each transaction. Always confirm the correct import structure with the relevant customs authority, a licensed customs broker, or qualified counsel before finalising a cross-border reseller shipment.