An importer with servers landing in early August is budgeting for a 10% surcharge that will not exist by the time the goods clear. On 24 July 2026, the Section 122 import surcharge expires by operation of law. Most of the market is being told the same thing about that date: do not celebrate, because a new Section 301 tariff is lined up to replace it. For the general importer, that advice is correct. For an importer of servers, networking hardware, or data centre equipment, it is wrong, and the difference is worth roughly ten percent of customs value on every shipment.

The Section 301 electronics exemption refers to the proposed Annex A exclusions in the 2026 Section 301 forced-labour action, which remove most IT hardware, including servers, computers, semiconductors, and telecommunications equipment, from the new tariff. Those goods lose the 10% Section 122 surcharge on 24 July without picking up a replacement duty. For technology importers it is a genuine reduction in landed cost, not the wash the wider market is bracing for.

The timing has a hard edge to it. A shipment of identical hardware entered on 23 July carries the 10% surcharge. The same shipment entered on 25 July may carry nothing. On a container of servers, that is the difference between a five-figure duty line and none at all, decided by the entry date.

What Actually Expires on 24 July

The Section 122 surcharge is 10% ad valorem, not 15%. That distinction matters because a great deal of commentary quotes the higher figure. The 15% is the statutory ceiling under 19 U.S.C. § 2132(a). An increase to that ceiling was announced in February but never enacted by proclamation, so the rate importers have actually been paying since 24 February is 10%, imposed by Proclamation 11012 and administered under HTSUS 9903.03.01. Our full guide to the Section 122 tariff sets out the structure and exemptions.

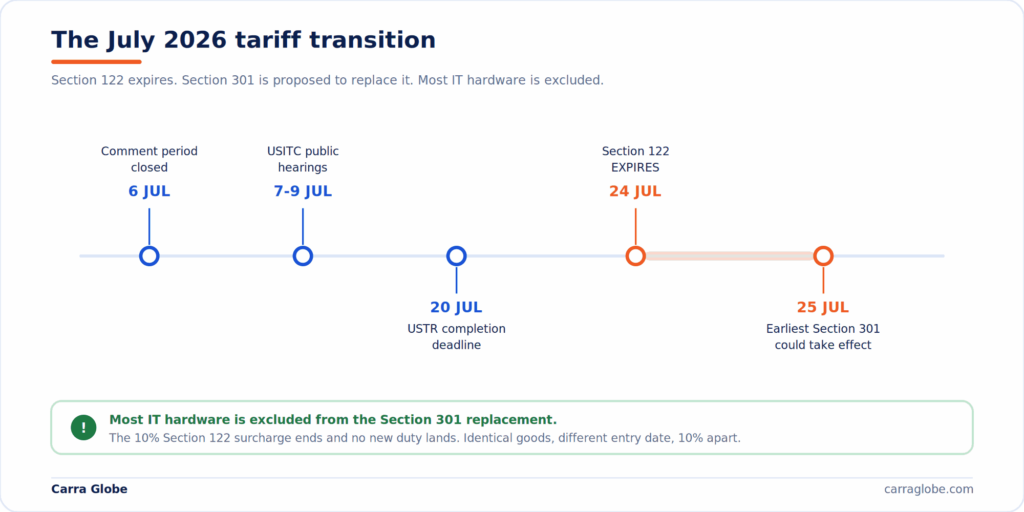

The expiry is not a policy decision. Section 122 permits a surcharge for a maximum of 150 days without an act of Congress. The clock started on 24 February. It runs out at 12:01 AM EDT on 24 July 2026. The President cannot extend it unilaterally, Congress has not passed legislation to extend it, and the surcharge therefore ends automatically. Whatever else happens, the 10% stops being collected on that date.

What Is the Section 301 Electronics Exemption?

On 2 June 2026, USTR issued affirmative determinations in Section 301 investigations covering 60 economies. Together they represent over 99% of US import value. USTR found that each had failed to impose or effectively enforce a prohibition on goods produced with forced labour.

The Federal Register notice proposes duties in two tiers. Economies that impose a prohibition, have committed to one under a reciprocal trade agreement, or operate a partial regime face 10%. The rest face 12.5%. The United Kingdom sits in the 10% tier, alongside Canada, Mexico, the European Union, and Taiwan. China, Vietnam, India, Japan, and South Korea sit at 12.5%.

The comment period closed on 6 July. Public hearings ran at the US International Trade Commission from 7 July. USTR is working to a completion deadline of 20 July, and the earliest the action could take effect is 25 July, one day after Section 122 dies.

The timing is not a coincidence. The investigations were initiated on 12 March precisely so that a successor would be ready when the surcharge sunset. The broader picture is covered in our guides to the Section 301 investigations and Section 301 tariffs in 2026.

Here is the part that changes the calculation for technology importers. The proposed action does not apply to every product. Annex A of the notice sets out exclusions, and two of them matter enormously:

- All articles already subject to Section 232 tariffs are excluded. This is an explicit de-stacking provision. The default rule in tariff law is that measures stack on each other. USTR has said the opposite here: if a good already carries a Section 232 duty, the new Section 301 duty does not apply on top of it.

- The Annex A product list itself covers electronics. The exclusion list includes computers, servers, semiconductors, integrated circuits, telecommunications equipment, smartphones, display modules, batteries, and semiconductor manufacturing equipment, alongside categories such as raw materials, pharmaceuticals, minerals, and aviation parts.

Put those two together and you have the Section 301 electronics exemption. An apparel importer loses the 10% Section 122 surcharge on 24 July and picks up a 10% or 12.5% Section 301 duty within days: a wash, or slightly worse. An IT hardware importer loses the same 10% and, if the goods sit in Annex A, picks up nothing.

What This Means for IT Hardware and Data Centre Importers

Does Section 301 Apply to Servers and IT Hardware?

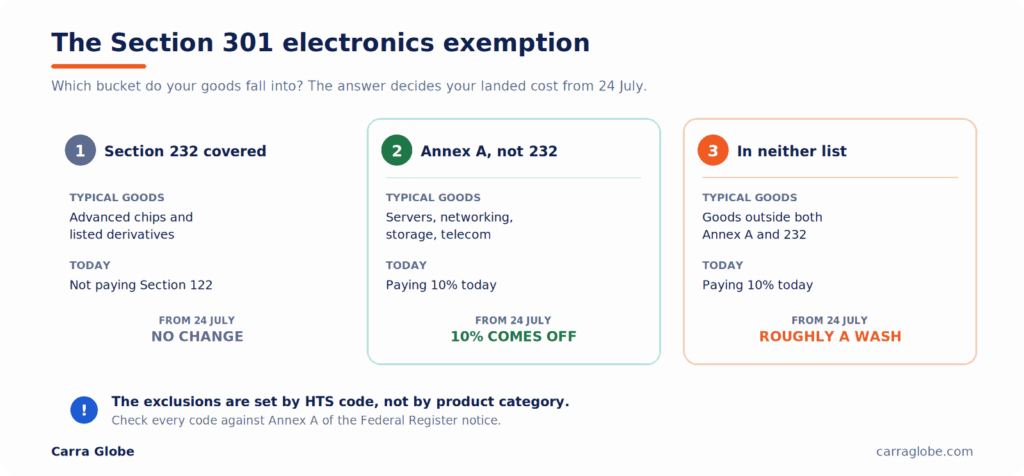

The entire cost shift turns on whether your goods fall inside the electronics exemption. The honest answer depends on which of three buckets a shipment falls into, and most importers have goods in more than one.

| Bucket | Typical goods | Paying Section 122 today? | Effect from 24 July |

|---|---|---|---|

| 1. Section 232 covered | Advanced computing chips and listed derivative products | No: Section 122 never stacked on Section 232 | No change. Section 232 stays. Also excluded from the new Section 301 |

| 2. Annex A listed, not Section 232 | Most standard servers, networking, storage, telecom equipment | Yes: 10% | The 10% comes off and no Section 301 replaces it. A real reduction |

| 3. Neither | Goods outside both lists | Yes: 10% | The 10% comes off, a 10% or 12.5% Section 301 lands. Roughly a wash |

The rule reduces to three lines:

- If the HTS code is already subject to Section 232, the new Section 301 does not apply, and Section 122 never did either. No change.

- If the HTS code is in Annex A but not under Section 232, the new Section 301 does not apply and the 10% Section 122 surcharge ends. A real saving.

- If the HTS code is in neither, the Section 122 surcharge ends and a 10% or 12.5% Section 301 duty replaces it. Roughly a wash.

Bucket 2 is where the electronics exemption does its work, and where most data centre hardware sits. On a USD 2 million shipment of servers and switching, the Section 122 surcharge is USD 200,000. If the goods are in Annex A and carry no Section 232 exposure, that USD 200,000 does not simply move to another line on the entry. It stops being charged. For a buyer running several such shipments through a build programme, the difference across a quarter is not a rounding error.

Shipping IT or data centre hardware into the US before 24 July? Whether your goods fall inside the exemption comes down to the classification on the entry. Carra Globe acts as importer of record for technology and infrastructure hardware across 175+ countries, classifying every entry correctly, claiming the exclusions that apply, and modelling landed cost on both sides of the date.

Bucket 1 is the one that surprises people. Importers of advanced chips and covered derivative systems often assume they have been paying Section 122 as well. They have not, because Section 122 never stacked on Section 232. Those goods see no change on 24 July, and the compliance layer around them, including export-control obligations, does not move either. Our guide to AI and GPU import compliance covers that layer in detail, and our guide to Section 232 on full customs value explains how the duty is calculated.

Four Catches That Keep This Honest

This is a proposal, not a settled rule, and a technology importer who budgets on it without understanding the qualifications is taking a risk. Four things could change the picture.

1. The proposal is not final

USTR explicitly invited comment on whether products listed in Annex A are appropriately excluded, and whether products should be added to or removed from the scope. The comment record closed on 6 July with hundreds of submissions, and the hearings have concluded. USTR can revise the annex, adjust the rates, or change the structure before it publishes a final rule. Until that rule appears, the electronics exclusion is a proposal that has survived a comment period, not a duty schedule you can bank.

2. Section 232 does not move

The 25% Section 232 duty on advanced computing chips and covered derivative products is untouched by any of this. It was not created by Section 122, it does not expire with Section 122, and the proposed Section 301 explicitly steps around it. An importer whose exposure is mostly Section 232 will see no relief on 24 July, and should not plan for any.

3. A second Section 301 investigation is still open, and it targets electronics directly

This is the catch that matters most for the medium term. Alongside the forced-labour investigations, USTR initiated a separate set of Section 301 investigations into structural excess capacity in the manufacturing sectors of 16 major economies. The sectors named include electronics, semiconductors, and batteries. That investigation has not yet produced proposed tariffs. If it does, the resulting duties would be a different action, carrying no obligation to repeat the Annex A exclusions, and could land on precisely the goods that the forced-labour action exempts. The relief described here is real, and it may not be permanent.

4. Section 122 is still in litigation

The Court of International Trade ruled Proclamation 11012 invalid on 7 May 2026. The Federal Circuit stayed that ruling on 11 June, finding the government likely to succeed, so collection has continued. If the surcharge is ultimately struck down, importers who paid it from 24 February onward may become eligible for refunds, a separate track from the expiry itself. The practical consequence is that entries filed now should be documented as if a refund claim may follow.

What to Do Before 24 July

- Map your HTS codes against Annex A. This is the step that decides whether the electronics exemption applies to you. The exclusions are code-specific, not category-generic. “Electronics” is not a qualifying description; a ten-digit code either appears on the list or it does not. Pull every active code in your catalogue and check it against the annex in the Federal Register notice. Our guide to HS codes for electronics and tech equipment is the starting point for getting those classifications right in the first place.

- Recalculate landed cost from 24 July, by bucket. A single blended assumption across your catalogue will be wrong, because different products land in different buckets. Model bucket 1, bucket 2, and bucket 3 separately. Our landed cost guide sets out the full duty stack.

- Look at entry timing. The surcharge applies to goods entered for consumption, or withdrawn from warehouse for consumption, before the expiry. Goods entered on or after 25 July may not owe it. Where a shipment is already close to the line, the entry date is a lever worth examining with your broker, though it should never be the reason to hold goods a buyer needs.

- Do not relax the compliance posture. Nothing here reduces classification, valuation, or export-control obligations. If anything, a duty saving that depends on an annex listing makes correct classification more important, not less, since the saving evaporates if the code is wrong. Our guide to reducing import duty in the US covers the legitimate mechanisms that survive the transition.

- Watch 20 July. That is USTR’s completion deadline. The final rule, when it appears, is what turns this from a proposal into a duty schedule.

Frequently Asked Questions

What is the Section 301 electronics exemption?

Annex A of the proposed Section 301 action excludes goods already subject to Section 232, and its product list covers computers, servers, semiconductors, telecom equipment, and batteries. Those goods would not carry the new duty.

The exclusions are specified by HTS code, so a product qualifies by its classification, not by being broadly described as electronics.

Does the Section 122 surcharge really end on 24 July?

Yes. Section 122 caps a surcharge at 150 days without an act of Congress. The clock started on 24 February and runs out on 24 July. The President cannot extend it, and Congress has not.

The rate that ends is 10%, not the 15% often quoted, which is the statutory ceiling rather than the rate charged.

Will my server imports get cheaper after 24 July?

If the goods sit in Annex A and carry no Section 232 exposure, yes: the 10% surcharge stops and nothing replaces it. If they already carry Section 232, nothing changes, since Section 122 never stacked on it.

Check the specific HTS codes rather than assuming the whole catalogue moves together.

Could the electronics exemption disappear later in 2026?

It could. A separate Section 301 investigation into structural excess capacity covers 16 economies and names electronics, semiconductors, and batteries. It has not yet produced tariffs, and carries no obligation to repeat these exclusions.

Treat the relief as real but not guaranteed to last, and keep modelling a second-wave scenario.

The market is being told to expect a handover on 24 July, and for most importers that is exactly what happens: one surcharge ends, another duty begins, and landed cost barely moves. For servers, networking, and data centre equipment, the handover has a gap in it, and the gap is worth about ten percent of customs value. Whether a given shipment falls into that gap comes down to a ten-digit code on an entry, which is the least glamorous and most valuable detail in the whole transition. The importers who benefit will be the ones who checked their classifications before the date, not the ones who worked out afterwards that they could have.

Disclaimer: This guide is for informational purposes only and does not constitute legal, customs, or trade advice. The Section 301 action described here is a proposal and had not been finalised at the time of writing. Rates, exclusions, and effective dates may change in the final rule. Always confirm your specific HTS classifications and duty exposure with the relevant customs authority, a licensed customs broker, or qualified counsel before making commercial decisions.